communication partner

communication partner

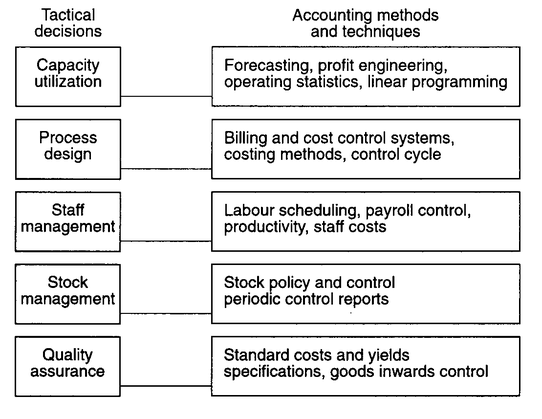

HIGHLY SPECIFIC METHODS IN CONTROLLING

Specific Methods are More Than Simple Techniques

Many accounting mistakes are made when real analysis starts to take place since estimates and economic indicators may change or be falsely interpreted. Productivity, activity and efficiency will be evaluated and relationships among financial statement items identified. Essentially, financial statement anylsis attempts to evaluate three key aspects of the business: liquidity, profitability, and solvency; however, some methods streamline information so that specific decisions can be made which separately or combined affect the three main aspects of financial information.